- When you can afford the payments: Regardless if you are buying an effective fixer-upper otherwise was remodeling a house you are located in already, you should afford the monthly mortgage payments. Look at the income and you will newest casing will set you back and you may estimate if or not there clearly was one move place within to include into an additional monthly expenses. You might make slices someplace else on the budget to cover the the brand new repair mortgage repayments.

- When your renovations boost your value of: When you cannot anticipate to recover the entire price of an excellent repair for those who end offering your home later on, it may be useful to find out if the renovate can make your house more vital, whenever so, exactly how much worthy of it does increase your home.

- In the event that remodeling is preferable to swinging: Oftentimes, it creates a great deal more sense locate and purchase a different house otherwise create a house out of scratch than simply it will in order to renovate your current possessions. Think of exactly how extensive the renovations will need to be so you can help your house be suit you before you proceed having a restoration mortgage.

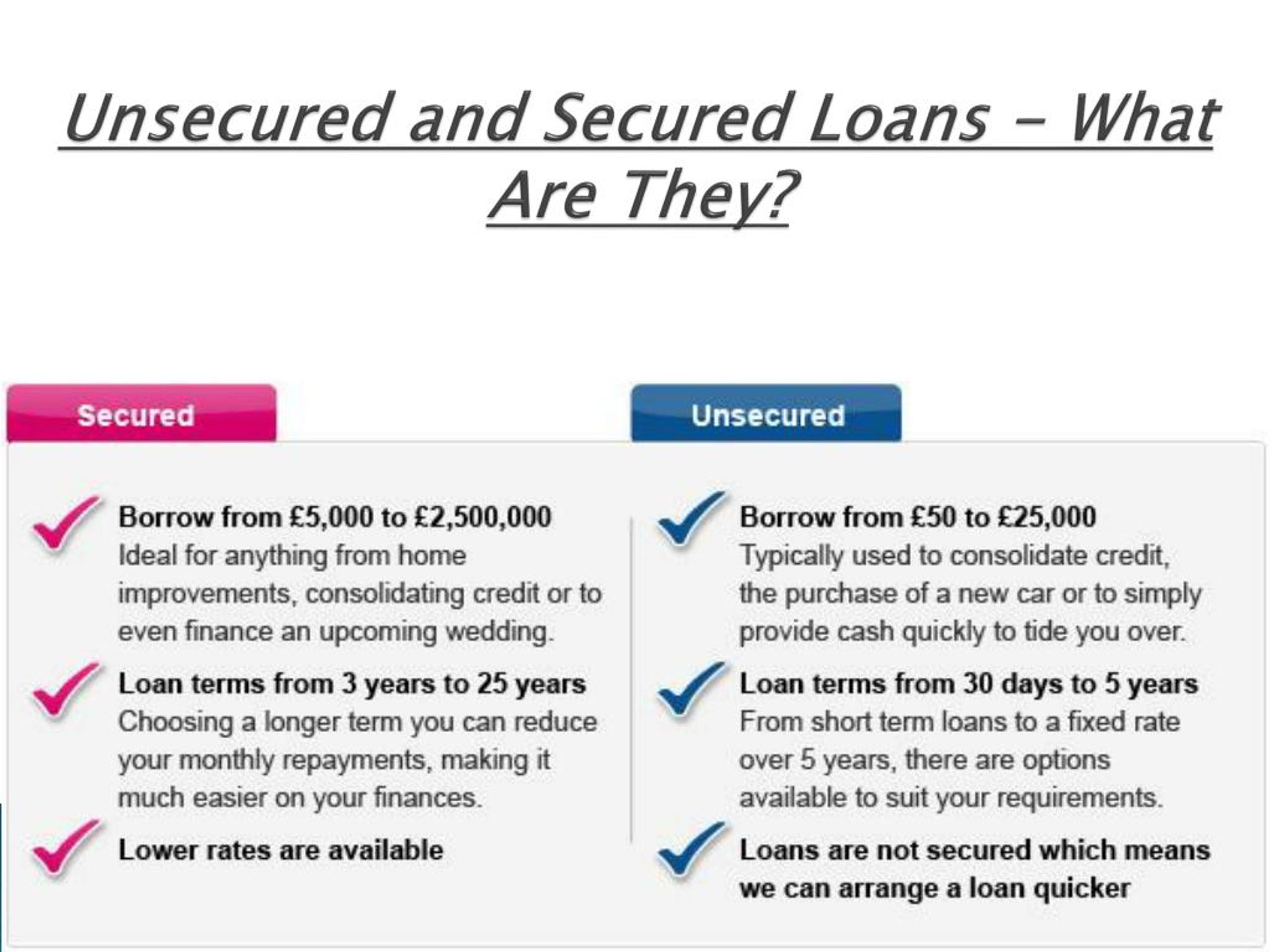

When you’re to order property that really needs some TLC, it creates sense to find out if you need to use specific of your mortgage to cover the cost of renovations. Oftentimes, you have the accessibility to carrying out that. However you need certainly to choose the right version of home loan. Extremely conventional home loans can not be always coverage the cost off renovations plus the residence’s cost.

To add the expense of restorations to your residence loan, you will want to select a repair mortgage. Up coming, when you submit an application for the loan, your use sufficient to safety the newest home’s price and also the cost of the newest renovation.

After you romantic into recovery home loan, the lending company pays owner brand new home’s sales rates. The rest of the borrowed count goes on the a keen escrow membership. Such, should your home loan try $150,100000 and family will cost you $one hundred,one hundred thousand, the seller will get $one hundred,100, while the remaining $fifty,100000 will go for the a free account.

The organization creating the latest home improvements will have accessibility the brand new escrow membership and will be capable remove payments from it because the work continues the project and milestones is actually achieved. The financial institution commonly find out if tasks are done up until payday loans Salt Creek the company becomes paid.

Exactly what Loan Is perfect for Home improvements?

How you can money renovations depends on numerous situations, including your current homeownership status, the newest restoration project’s cost, and your credit history. View some of your loan options.

1. Build Mortgage

Even though many someone score a casing financing to purchase rates of making a property from the ground up, you can also find a houses financing to purchase will set you back out-of renovating an existing home. Whilst the application procedure is comparable, a housing mortgage is actually slightly distinctive from a home loan. To find the financing, you should promote evidence of money and you may go through a credit have a look at. you will need to make a down-payment for the loan.

If you decide to get a homes loan to pay for household home improvements, you may want and come up with a bigger advance payment than your carry out for a vintage mortgage. Always, loan providers assume borrowers to place at the very least 20% off after they finance renovations otherwise new framework. Also, truth be told there rate of interest into the a homes financing might be greater than the attention recharged to have a traditional mortgage.

Pursuing the restoration is finished, a casing mortgage have a tendency to generally become a home loan. It does do that automatically, or you could need to go from the closing process once again.